UK Consumer Trends in 10 Charts

Issue 83 l Eka’s Weekly Roundup (30 July 2024)

We’ve been trying to understand how the consumer landscape is changing in the UK. We will be publishing a larger note in due course, but wanted to give you a teaser of what we’ve found so far.

Building a consumer startup over the next 10 years will require different strategies to those in the past 10 years. So what’s changed?

Customer acquisition costs are much higher than they were. One estimate suggested customer acquisition costs have risen +222% between 2013-22.

Building tools have evolved. Think of inventory management with Katana, subscription support with ReCharge, and marketing software with Clevertap.

Inflationary pressures in the supply chain proving to be stickier than initially hoped.

The macro picture has undeniably shifted from the ZIRP* era. Consumers are being squeezed and becoming price sensitive.

Innovators in climate & health can harness new strategies for the next Consumer era. These include the power of community to drive organic traffic, harnessing offline channels to enable reacquisition, or using novel technologies to unlock better consumer experiences.

As part this UK Consumer work, we’re conducting our largest mapping to date. If you’re building consumer-facing sustainability or health, we’d love to hear from you!

Feel free to reach out at estia@ekavc.com ⭐️

*Zero Interest Rate Policy.

UK Consumer in Three Parts 🗞️

Part 1: The macroeconomist’s view 🏦

1. UK inflation: overall inflation measures have passed their peak, but rental inflation is running high.

CPIH is consumer inflation including housing costs, while CPI excludes housing costs. OOH is owner occupied housing inflation, so CPIH = CPI + OOH. This is now largely in line with our European peers like France and Germany who are seeing c2% inflation. Some notable callouts outside the bounds include Finland at 0.5% and Belgium at 5.4% (see note here).

2. Retail sales are still down on the 2019 baseline, but have found a floor in early 2024.

Retail sales data indexed to June 2019 (i.e. June 2019 = 100). The initial recovery in 2021 faded throughout 2023 and 2023 into negative territory on 2019, but the data in early 2024 looks stable.

One interesting cut within this is internet sales which look to actually be creeping back up slowly since their initial jump around the Covid-19 pandemic. Different retailers are benefitting to varying amounts (see Boohoo having their e-comm sales be down -9% year over year while Amazon is up +7%).

3. & 4. Energy costs are so last year: power prices come down from peaks.

Early data from 2024 suggests that energy costs across gas and electricity are still elevated on 2019 but have come down from their peaks during the crisis between 2022-2023.

Same message, different numbers. Gas inflation rates have come down from their highs and were in negative territory in January 2024.

5. If energy is out, then housing costs are in. Rental costs are going through the metaphorical roof.

One of the key inflation drivers now is housing and rental costs within the UK. To go deeper, read Rightmove’s Rental Trends Tracker from Q2 which covers asking rent in Greater London and exc. Greater London - inflation isn’t where you might initially think it is!

6. Food pricing is coming down on for every day staples, but cafes & restaurants are well above the average.

Inflation rates on food peaked close to 20% in 2022-2023, and has since come down but is still rising 7% year over year.

Going out for food and drink is seeing high levels of inflation and is still rising 8% as of January 2024.

One of our favourite stats in pulling this newsletter together: “It costs around £12.77 for this dish to be enjoyed at Whiteheads Fish & Chips, a chippy that won the title ‘Fish & Chip Takeaway of the Year’ in 2023. This price is 40.48% higher than in 2013 and 1476.54% higher than 50 years ago”.

Part 2: The household view 🏘️

7. The average UK household spends £528 each week, with housing leading in the mix.

This has come up as part of the total spend mix in recent years (see the inflation charts if you want to better understand why).

8. Disposable income has been moderately trending up while expenditure hovered around £600 / week*.

A Finder survey estimated that 59% of those between 25-34 year olds in the UK have less than £1k in savings, and the average saving in that age range is £3,800.

9. For the bottom fifth of UK households by socioeconomic background, housing costs are almost 25% of total spend.

Same as above. One Money Advice Survey estimated that half of UK households wouldn’t be able to cover an emergency £300 payment.

Part 3: The kitchen table view 🍳

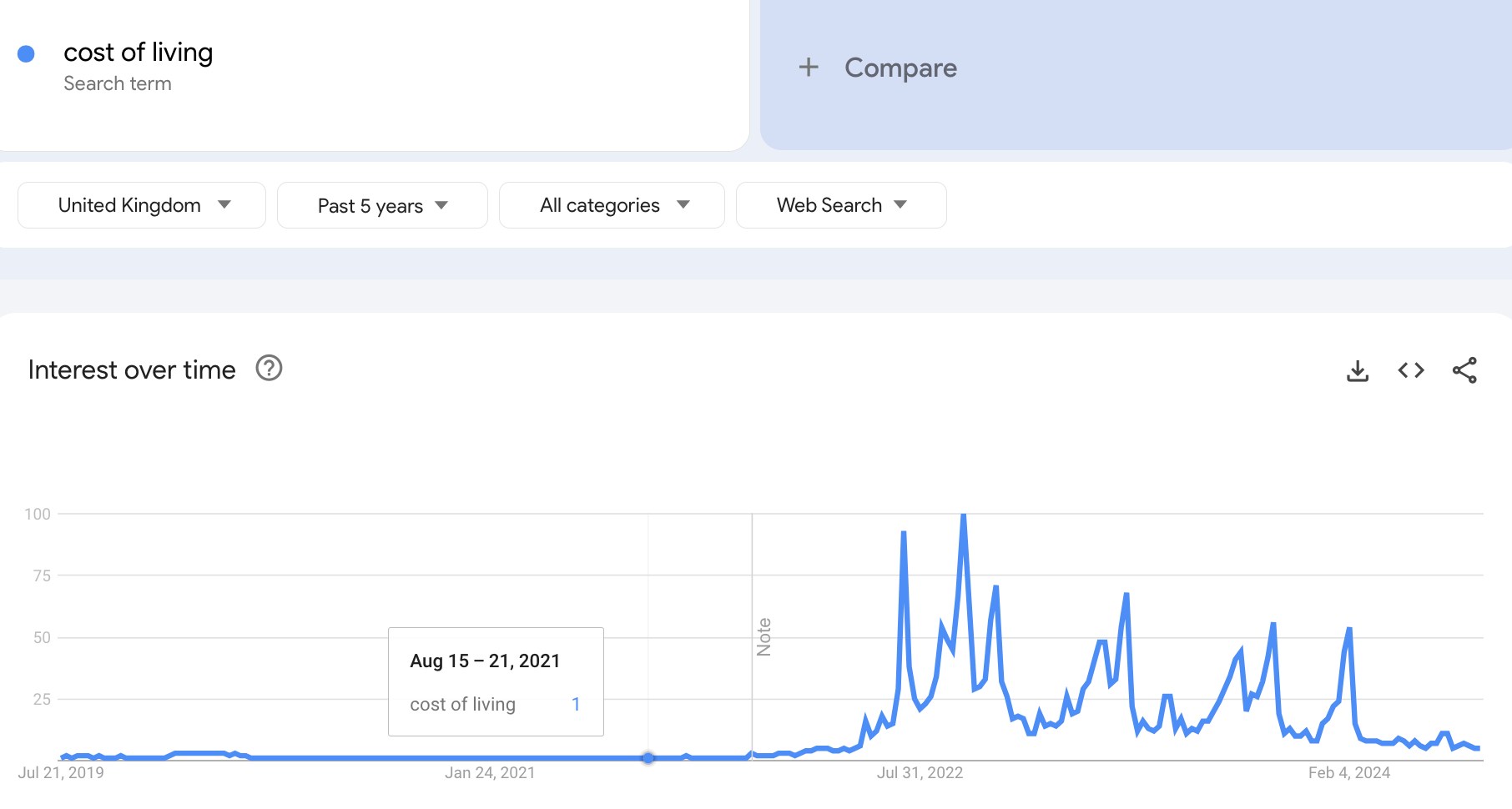

10. Has the consumer interest in cost of living blown over?

The consumer interest in cost of living seems to have dwindled. Is this a long or short term trend?

Reflections for Impact Innovation

Price competitiveness (health & some climate). Price competitiveness relative to incumbents matters more than ever when building in this new era. From an impact lens, this is essential to 1) ensure health equity to those who can’t afford basic life-essential products and 2) consumers who may not be able to afford a green premium for a sustainable alternative.

Cost curve innovation (mainly climate). When price competitiveness is not possible, as is often the case in the early stages of pricing, then a clear and sensible roadmap to price innovation should be thought through. Think of Tesla’s pricing over time from a luxury brand to an increasingly mass market product, or Whoop’s early revolution in personal wellness.

Superior consumer experience (health & climate). We’re always excited to see the enabling of genuinely better consumer experiences using technological innovation in both of our impact areas (climate & health). We believe that technological shifts are the enablers to 1) a circular and decarbonised system, and 2) a predictive, proactive, and preventative health system.

As mentioned towards the top, we’re building our knowledge across consumer verticals including fashion, food, wellness, and health. Please get in touch you’d like to chat 👋

Week in Impact Articles ✍🏽

Monday: Many used EVs in the UK are now equal to, or lower in price than, petrol equivalents

Tuesday: Why Stopping Algorithmic Inequality Requires Taking Race Into Account

Wednesday: Great British Energy Founding Statement

Thursday: Will the new government pass the test of leadership on health inequalities?

Friday: GPT-4o mini: advancing cost-efficient intelligence

3 Key Charts 📊

1. If energy is more affordable than gas, then the case for heat pumps becomes much higher

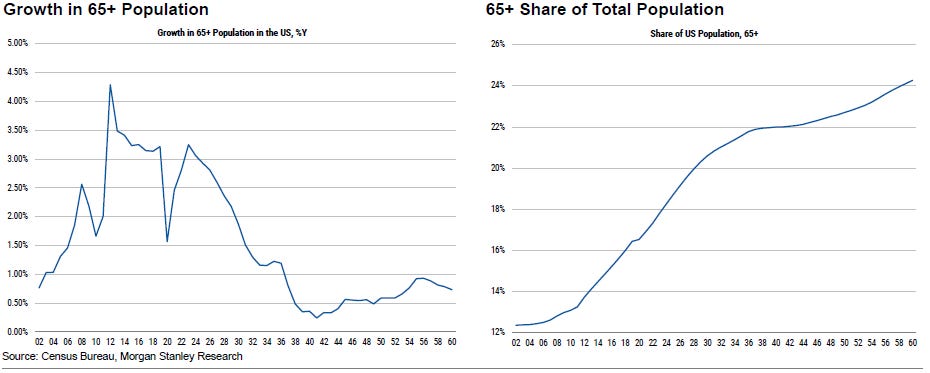

2. Ageing is more than just a Biden thing

3. The smaller, the cheaper, the more energy efficient?

Getting in Touch 👋.

If you’re looking for funding, you can get in touch here.

Don’t be shy, get in touch on LinkedIn or on our Website 🎉.

We are open to feedback: let us know what more you’d like to hear about 💪.

Very underestimated substack by Eka.