Eka’s Weekly Roundup (30 September 2022)

Issue 2 l Consumer Subscription Services

Welcome to our second edition of Eka’s impact newsletter 🥳!

We invest in early-stage technology businesses with either 1) environmental and/or 2) social impact at the core of the business. This newsletter will be focussed on tracking interesting stories across these themes in the UK and Europe 🌎.

For this second edition, we spend some time looking at GP Bullhound’s 2022 Consumer Subscription Software report that they released earlier this week. Eka is a strong believer in consumer’s potential to drive environmental and social impact. We believe that core consumer principals from models like e-commerce and gaming should be applied to mission-driven health and climate companies.

State of Consumer Subscription Software 🗞️

This week, the team was reading GP Bullhound’s 2022 Consumer Subscription Software report. The report is a broad overview of the state of CSS: from growth, to market structure and marketing dynamics. We are positively encouraged by the structural shift in app usage away from just games towards highly functional non-game models. We believe these are an exciting way to promote systems change from both an environmental and social impact perspective (see Why We Invested in Paired as an example for how our portfolio companies are replicating this model). We pull out the bits from the Bullhound report that interested us the most below.

Reminder of how we got here

Consumer subscription apps have been growing steadily over the years. In Q2 2016, there was only one app on the US App Store that was generating >$50m in consumer spending. Fast forward to today and there are 12 that meet this threshold (notably Bumble, Flo, Youtube, and Strava).

Interestingly, the market had previously been dominated by games related applications. These were roughly two-thirds of App Store spending five years ago. Recently though, these have been overtaken by non-games which now account for >50% of total consumer spend on the US App Store. This suggests we are starting to see the transition to genuine functionality through apps. It’s for this reason that we are bullish on the potential impact of apps on health and climate given the real opportunity to create positive system change.

CSS and market structure: how to win

The report mentions winner-takes-all structures drive value in CSS businesses. Monopolies in small markets can be lucrative, while large TAM plays require strong differentiation and competitive moats.

While we think this is largely the case, we believe CSS are not winner-takes-all but rather winner-takes-most, with ample space for innovation around vertical specialisations and different customer segmenting. This is especially the case in non-games companies where going after a category may require multiple different approaches. Additionally, we believe that highly capital-efficient businesses (especially in the current funding environment) have a strong competitive advantage against those that more intensive.

The chart below from the report outlines how CSS businesses create their flywheel using data, monetisation, churn management, and content. This is a great summary of effective competitive moats.

Craigslist is the mother of invention

This also reminded us of Rex Woodbury’s post this week on unicorn marketplace businesses coming from similar models. CSS models have arguably also gone through this transition (and are still going through it!).

Let’s apply this to CSS businesses. The personals category is replaced by Bumble and Match Group. Entertainment is replaced by Spotify and Netflix. Fitness is replaced by Peloton and Apple Fitness +.

Putting numbers around it: best-in-class benchmarks

We thought the most helpful part of the report was around benchmarking key consumer subscription KPIs such as renewal rates and churn. We recommend reading this section in detail for detailed descriptions of the below KPIs.

As a summary, we show ‘worse to best’ ranges for various benchmarking criteria.

Annual user growth rate: <50% to >100%

Gross margins: <60% to >90%

1st pay period churn rates: >50% to 20%

Free-to-paid conversion rate: <2% to 10%+

Sales efficiency ratio: <0.5x to 2.0x

LTV/CAC:* <3x to >6x

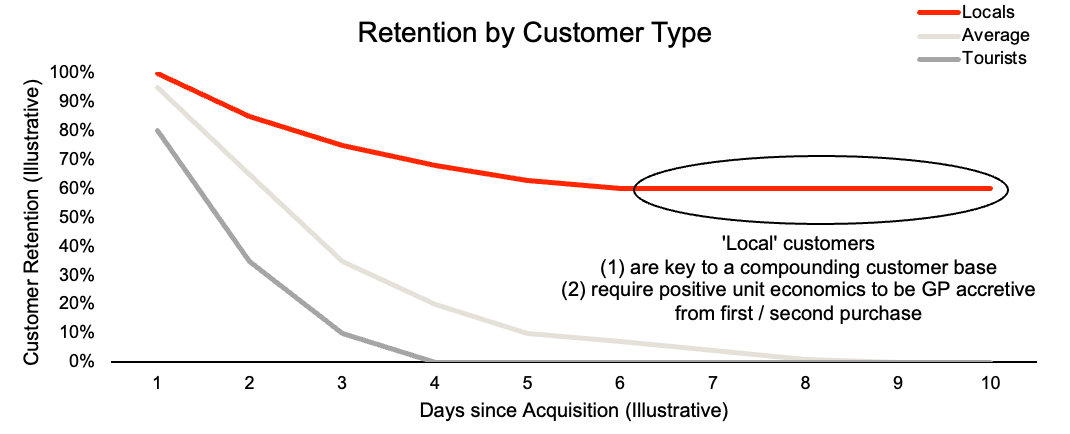

It’s worth spending a bit more time on what good LTV/CAC means. There is usually quite high churn in the first few days and weeks in CSS businesses. For this reason, we should be looking at long running retention, usually around 1 month (but can be 3, 6, or 12 months depending on the billing cycle). See chart lower down for a more qualitative description of retention rates.

A short CAC payback duration is important to combat high churn rates at the start of the retention curve. Ideally, this should be paid back on the first purchase so that no purchase is loss making. Payback can be flexed depending on typical frequency of purchase as well as the size of the ‘sticky’ customer base (note Hellofresh’s low retention but incredibly high customer volume).

The report also introduces the concepts of Locals versus Tourists. We think this is a really helpful way of conceptualising how sticky the proposition is. This is a function of stickiness of 1/ market (macro-level) 2/ product (micro-level) 3/ business (corporate-level).

More practically, there are also charts around low, median, and high renewal rates across various industries for annual and monthly subscriptions. As seen, the average annual renewal rate is around 30% with best in class being >60%.

This trend is higher for monthly subscriptions, with the median being closer to >60%. As expected, the relative industry trends broadly follow the annual shape above.

(Small) note on inflation

Finally, it’s worth pulling out the section on inflation. Subscription services have been under the spotlight (Netflix) in recent months as being the first to be cut as consumers wallets get pinched. The share of subscription cancellations due to cost has gone from 2% in October 2021 to 22% in March 2022, and is likely much higher now.

The majority of overall cancellations are coming from younger generations, with cancellation rates in Gen Z’s and Millennials being at 17% and 16% respectively, compared to 14% for Bridge Millennials and 11% for Gen X.

Wrapping up: an exciting report!

This has given us quite a lot of food for thought. We are generally excited about the CSS space in our investment pipeline, and are encouraged by the hard numbers around best-in-class. For any other CSS keen beans, this is a great coffee-break read!

3 Key Charts 📊

1. Displacement between investment and emissions

2. There is a $711b biodiversity funding gap

3. Increasing affordability of solar versus wind

Deal Capture 💰

Deals in the impact space across the UK and Europe

Carbonfuture

Carbon credit business Carbonfuture raised €5.5m. Led by Carbon Removal Partners, Ubermorgen Ventures, and WiVenture.

Cemvision

Sustainable cement company Cemvision raised €2m. Led by Polar Structure and Backing Minds.

Connected Kerb

EV manufacturer Connected Curb raised £110m from Aviva investors.

Innomy

Mycelium-based meat producer Innomy raised €1.3m in a pre-Series A round.

Papaya

Last-mile logistics software company Papaya raised $3.5m. Included institutional and angel investors.

Peachy

Health insurance business Peachy raised £1.50m. Led by angel investors.

PlanetWatchers

Environmental data analysis business PlanetWatchers raised £10m in its Series A. Co-led by Seraphim Investment Trust and Creative Ventures.

Woltair

Sustainable energy company Woltair has raised €16.3m. Led by ArcTern Ventures.

Next Week… 📅

… we’ll be looking out for AdaCon and Tech Nation x Net Zero.

…Upcoming Events… ⌛

… you can catch us at in the not-too-distant future.

Tech Nation x Net Zero - October, 6 October.

… and Getting in Touch 👋.

If you’re looking for funding, you can get in touch here.

Don’t be shy, get in touch on LinkedIn or on our Website 🎉.

We are open to feedback: let us know what more you’d like to hear about 💪.