Eka’s Weekly Roundup (3 March 2023)

Issue 20 l What's a tonne of carbon worth?

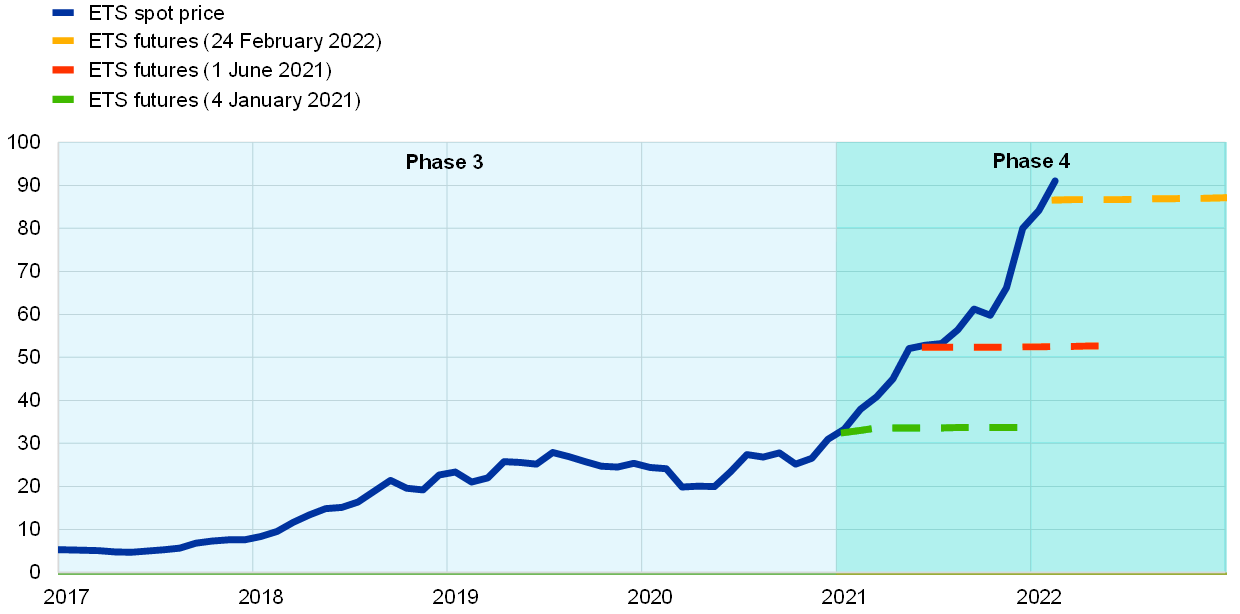

The EU’s price of carbon has topped €100. The European carbon trading market started back in 2005, and now covers around 40% of GHG emissions from the block. Last week, the price of one carbon credit reached new highs following a period of cold weather, wider energy disruption, and increased hedging demand. We take a look at the history behind the scheme and what the pricing developments mean for the carbon market.

Carbon crosses the €100 chasm 🗞️

This chart was all over the media last week - we take a look at the history behind the carbon markets and what’s been pushing up pricing.

Quick history of carbon trading

Carbon trading started in 1997 at the Kyoto Protocol. This created four types of credits:

Assigned Unit Amounts

Removal Unit

Emissions Reduction Unit (ERU)

Certified Emission Reduction (CER)

Inception: The largest emissions trading market was launched back in 2005 by the EU Emissions Trading Scheme. Pollutant credits were given to companies for free to encourage uptake during the trial. From 2006, the price collapsed from $32 down to $9. Managing supply was quite volatile in the first few years of trading, with high variability between 2006 to the mid 2010s.

Early Growth: In 2013, a benchmarking approach was created to allocate free allowances based on existing carbon emissions. This benchmark then decreases year-on-year, decreasing the cap for total carbon credits and increasing demand. The aim is to encourage sectors to gradually swap out their carbon-emitting practices as the allowable trading cap decreases. The EU also banned the purchase of CERs and ERUs by participants unless the projects were in LDCs.

Modern Day: In December 2022, the European Parliament and Council wrapped up a revision of the Trading Scheme (EU ETS) and increased the target of cutting GHGs by -62% by 2030 from a 2005 baseline. The revised scheme will phase in new sectors like the maritime industry between 2024 to 2026.

The current obligations cover 1,000 installations across the UK, including:

power stations

oil refineries

offshore platforms

iron and steel manufacturing

cement and lime producers

Pricing depends on the trading market (below), with the EU ETS seeing high inflation in early 2021. This has now passed the >E100 mark.

Determinants of carbon pricing

EU ETS are allocated in the market via a mixture of free allocations and auctions. One credit is equivalent to the right to emit 1 tonne of CO2. There are a few key flexors in carbon pricing.

Supply. As the ETS scheme matures, free allowances are reduced so that the total allowable cap shrinks. Over time, the pricing model will move to a auction based model. For example, aviation will see a full auctioning of allowances by 2027 to create a stronger price signal around emissions reduction.

Energy mix. The cooler weather and low wind power output this winter meant that companies needed to ramp coal and natural gas power generation. Consequently, they needed to buy more carbon credits given the changing energy mix (Grist). The scheme can also favour richer countries like France which naturally rely less on natural gas & coal compared to poorer countries like Poland with high fossil fuel dependency.

Hedging. Utilities can hedge their exposure as supply and energy mix change. This can push up pricing indirectly (FT).

Regulation. The 2021 regulatory change cemented the role of EU ETS as the EU’s major decarbonisation tool, encouraging more trading and speculators to enter the market.

Futures markets. The futures markets have been relatively flat relative to the spot price. There is not a high cost of storage and no tangible benefit to holding allowances in the same way there is for physical commodities.

Where to next?

The community is split in two following the price increase.

Glass half full

The optimists’ view is that increased pricing is creating a real incentive to shift from fossil fuels to renewable power generation. This would help high capex projects like carbon capture & storage or hydrogen deployment. Higher pricing was always going to be the end state of the EU ETS scheme, and corporates have a relatively transparent view of where those caps were trending.

Papers have shown that the EU ETS has also materially decreased emissions since implementation (chart below, link to paper here). Some of this may be due to carbon leakage, which is when companies offshore their emissions, but directionally the trend line is encouraging.

Glass half empty

The pessimists’ take is that this decreases the EU’s price competitiveness for manufacturing sectors. This is particularly strong in steel manufacturing which has seen its pricing increase significantly following the energy crisis.

Carbon credits can also give a distorted view of reducing emissions, as published by Zeit a few weeks ago (see Disney’s balance sheet below). These aren’t directly tied to EU ETS schemes but the logic is similar.

Washing it out

The high price volatility in the EU is quite extreme compared to other trading blocks (see chart above). Looking out, policy makers and traders will need to weigh up the balance between 1) speed to transition and 2) financial nudges to change emitting behaviour.

In the long run, we believe that buying off emissions won’t be a sustainable solution at the systems level. Instead need to focus on scaling carbon storage, removal, and circular processes to fully decarbonise the economy.

3 Key Charts 📊

1. Life expectancy in the US slides post pandemic

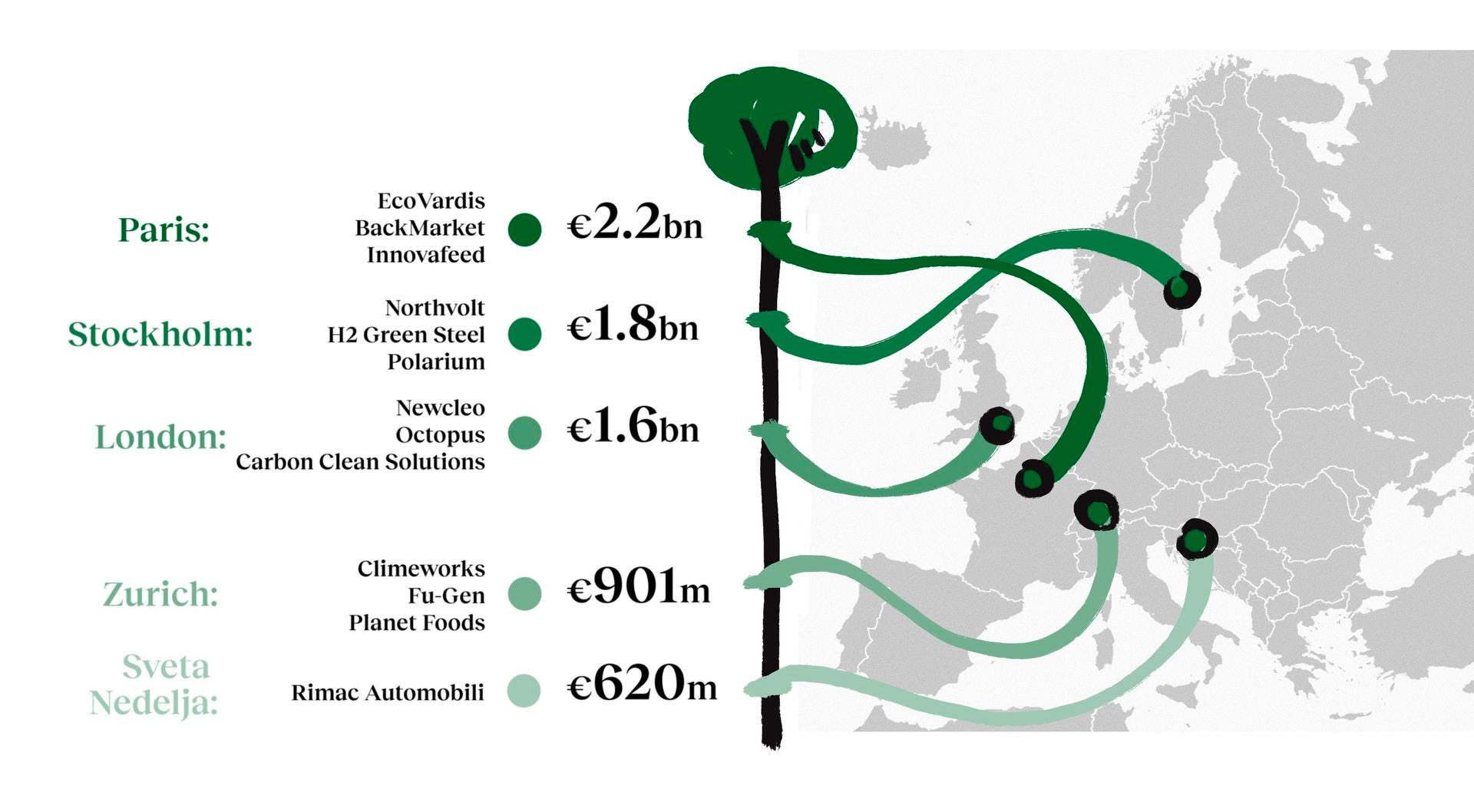

2. Mapping out climate investment across Europe

3. How Tesla is becoming an energy retailer

Deal Capture 💰

Deals in the impact space across the UK and Europe

Doctorly

Health tech startup Doctorly raised $10m in a Series A. Included Speedinvest and Calm/Storm ventures.

Hectare

Farming SaaS company Hectare raised £17m in a Series A.

Inarix

Agtech startup Inarix raised a €3.1m seed round. Led by Ankaa Ventures.

Pili

Sustainable pigment company Pili raised a $16m Series A. Led by BPI France.

Powervault

Battery storage Powervault raised £4m. Led by Green Angel Syndicate.

Getting in Touch 👋.

If you’re looking for funding, you can get in touch here.

Don’t be shy, get in touch on LinkedIn or on our Website 🎉.

We are open to feedback: let us know what more you’d like to hear about 💪.