Eka’s Weekly Roundup (27 January 2023)

Issue 16 l State of Carbon Removal

Carbon dioxide removal (CDR) is an important tool to get us to net zero. CDR is in all scenarios which meet the Paris temperature goal. We at Eka have long been promoters of the CDR space, having published this primer on it almost two years ago. Alongside our portfolio company Sourceful, we then developed an open source directory of CDR companies called Carbon Removers, where you can subscribe to stay up to date with the latest companies added.

Oxford University put out the first comprehensive report on the State of Carbon Dioxide Removal earlier in January. Today, almost all removal comes from ‘conventional’ techniques: afforestation, reforestation, and management of existing forests. To get to the 1.5C pathway, we require novel technologies like bioenergy carbon capture & storage (BECCS), biochar, and other novel removal methods. These need to grow at least 1,300x by 2050. This deployment gap must be solved by a few stakeholders (financiers & regulators), though there are substantial differences across solutions and geographies.

Carbon under lock and key 🗞️

🌎 Setting the Scene: What is CDR?

CDR technologies involves a few key components.

CO2 must be captured from the atmosphere (not from fossil fuels)

Storage must be durable so that CO2 is not soon reintroduced into atmosphere

Removal must be a result of human intervention (incremental to Earth natural process)

The diagram above better illustrates the three principles of capture, storage, and incremental process. This is different to CCS (carbon capture and storage) which can look at fossil fuels. CDR is also different to CCU (carbon capture and utilisation) as CCU can release CO2 back into the atmosphere relatively quickly after being inserted into new carbonated drinks, fuels, and plastics.

Storage timescales vary greatly by storage source. These are also affected by external human activity such as land use and maintenance.

🏭 Mitigation and cost potential by technology

There are varying estimated costs at scale for technologies. Today, the cheaper solutions include soil carbon sequestration, reforestation, and rock weathering. There are several unknowns for other nature-based solutions.

Mitigation potential has even greater variability between methods. Ocean alkalinisation has an upside potential of 100 GtCO2 per year, which could render it one of the most cost effective solutions. Most other solutions are closer to removing 10-20 GtCO2 per year. Again, research is early here so these numbers should change over time.

The report also notes varying technology readiness levels (TRLs). These are mainly qualitative assessments, with novel technologies (DACCS, BECCS, Biochar) ranking lower than nature-based solutions like agroforestry and improved forest management.

🌡️ Fitting into the Paris temperature goals

To date, most of policymaking has been focussed on conventional CDR methods through forestry and agriculture. Attention is turning to more novel forms of CDR in the UK and US. Below, the report estimates gross emissions vs. gross removals from 2010 to 2100 in order to get to net zero, split by conventional and novel methods.

Estimations for required deployment vary greatly across pathways to get to 2C or lower, ranging from 450 to 1,100 GtCO2. Interestingly, conventional CDR methods is responsible for 78-100% of CDR in 2030 in both 1.5C and 2.0C pathways according to different estimates. Novel CDR methods increase as part of the mix throughout the century (but not significantly before 2040-50).

🔍 Looking to the future: potential to scale

The chart below shows the growth trajectories of three CDR methodologies. this involves both announced and built capacities from industry and businesses. The shaded segments show how the last known year of capacity announcements fits into the high and low assumptions the 2050 goals.

We can extrapolate current deployment rates, which will be an underestimate relative as this ignores new project deployment beyond 2025. BECCS could see 31-209 MtCO2 per year of deployment, 7-298 MtCO2 of DACCS, and 2-65 MtCO2 of biochar. This still requires a substantial acceleration in innovation pace and scope.

3 Key Charts 📊

1. Insurance losses related to climate are rising

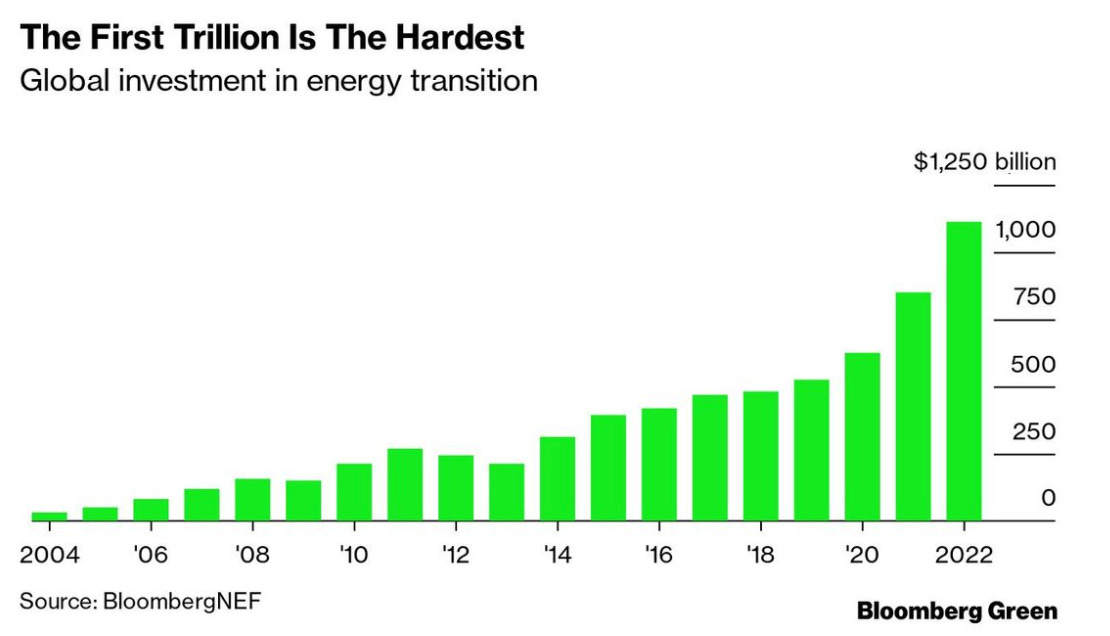

2. Global investment in energy transition hits $1tn

3. Reflecting on startups and valuation cycles

Deal Capture 💰

Deals in the impact space across the UK and Europe

Renaissance Fusion

Nuclear fusion startup Renaissance Fusion raised a €15m seed round. Led by Lowercarbon Capital.

Slingshot Simulations

Digital twins company Slingshot Simulations raised a £3m Series A. Included Northern Gritstone and Mercia.

Unwasted

Cardboard construction company Unwasted raised £1.5m. Led by Elbow Beach Capital.

Waire Health

Remote monitoring company Waire Health raised £2m. Led by Eos Advisory.

Wayout

Water treatment company Wayout raised a €6m Series A. Led by Copenhagen-based Climentum Capital.

Getting in Touch 👋.

If you’re looking for funding, you can get in touch here.

Don’t be shy, get in touch on LinkedIn or on our Website 🎉.

We are open to feedback: let us know what more you’d like to hear about 💪.