Eka’s Weekly Roundup (21 October 2022)

Issue 5 l Signposts from public markets

Welcome to our fifth edition of Eka’s impact newsletter.

As we go into Q3 reporting for public companies, we thought it was worth signposting which results will matter for the private markets. These results provide useful signals which can help guide our thinking and investment, especially for those looking at consumer-facing companies. We list the most important areas that we will be watching out for, including advertising, discretionary retailers, non-discretionary retailers, and digital healthcare (a varied bunch 😊).

Signals from Public Markets 🗞️

📱 Advertisers

Advertisers play an important role for early-stage companies, specifically around CAC competitiveness. Early indications for 2022 have been that companies which raised during the height of the market (2019-21) have experienced high levels of CAC inflation which is eroding the path to profitability. Hims and Hers saw increasing CAC according to their Q2 report for example, but more generally this article suggests CAC has gone up 60% in the last five years. Snapchat for example posted results yesterday with higher user numbers but decreased revenue. Understanding how demand for advertising is changing will be important when forming a view around CAC/LTV for future investments as well as tracking our portfolio’s performance more generally.

Key question for us: How is CAC trending given advertising spend?

Companies which matter: Alphabet, Meta.

Reporting dates: Alphabet (Oct 25), Meta (Oct 26).

👜 Discretionary Retail

Given the cyclicality of discretionary retail, we will be looking for current data around consumer health as well as sentiment going into the end of the year. Customer demand so far has held up relatively well given the macroeconomic headwinds, so seeing if that starts to turn into Q3 will be interesting. The early releases in the UK and Europe we have seen in recent weeks suggest that sentiment is becoming more negative into winter. Discretionary retail is a wide and broad category, so we illustrate just a few companies below that we’ll be looking out for.

Key question for us: How pinched are customer wallets today, and what are the early signs of health into 2023?

Companies which matter (a bunch!): Cineworld, Estee Lauder, Greggs, Nike, TJX Companies, Zalando and more…

Reporting dates: Estee Lauder (Nov 1 estimated), TJX (Nov 16), Nike (Dec 19 estimated), Zalando (3 Nov) Greggs (TBD), Cineworld (TBD).

🛒 Consumer Staples

A better sense of customer health will be seen through consumer staples (goods that you buy every day). We will also be interested in 1/ how customers trade down, 2/ whether pricing is the most important determinant in decision making, and 3/ the degree to which sustainability, quality, and convenience take a hit.

Key question for us: How impacted will the most resilient customer goods be during the incoming recessionary period?

Companies which matter (also a bunch!): Colgate, Nestle, Philip Morris, Unilever.

Reporting dates: Philip Morris (Oct 19 estimated), Unilever (Oct 27), Colgate (Oct 28), Nestle (Feb 16 2023).

💊 Digital Health

One of the most strongly over-weighted sectors is healthcare currently, according to a BofA report. However newer digital health companies have had rockier starts recently for a variety of reasons (digital health efficacy, user growth…). While we don’t think Q3 is the turning point here, we will be looking for profitability and growth trends across the newer public digital health companies.

Key question for us: How is user behaviour changing (or not) in terms of retention and frequency?

Companies which matter: Babylon, Cue Health.

Reporting dates: Babylon (Nov 10), Cue Health (Nov 10 estimated).

3 Key Charts 📊

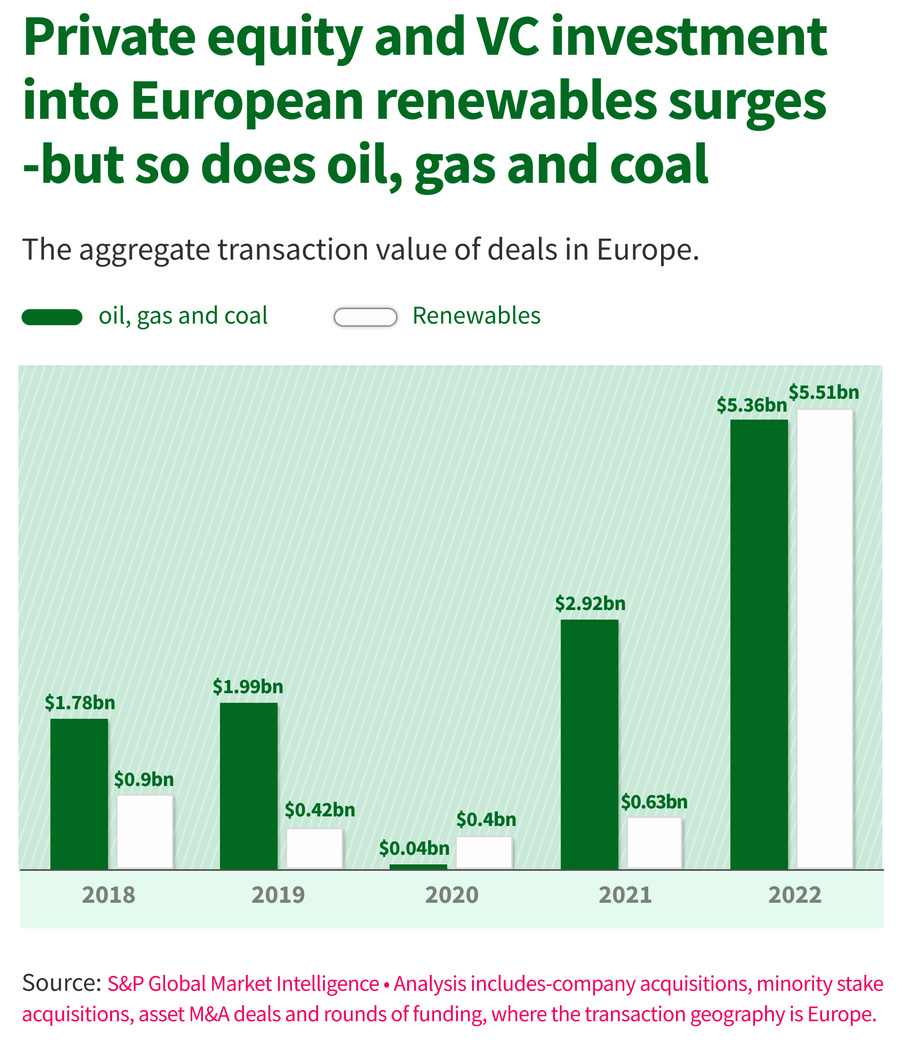

1. Comparing private investment in energy shows an encouraging trend on a mix basis

2. Apps per company have grown significantly

3. Renewables are getting more and more traction globally

Deal Capture 💰

Deals in the impact space across the UK and Europe

BlueSkeye AI

Mental health platform BlueSkeye AI raised £3m. Included Foresight VCT and Praetura Ventures.

Climateiq

Carbon accounting platform Climateiq raised €6m. Led by Singular and Cherry Ventures.

Ecoligo

Solar energy startup Ecoligo raised a €10m round. Included Fotowatio Renewable Ventures.

Enhanc3d Genomics

Functional genomics company Enhanc3d Genomics raised a £10m Series A. Led by BGF and Parkwalk Advisors

Levidean

Hydrogen startup Levidean raised a £12m round. Led by Baker Hughes.

Liquid Wind

Methanol fuel company Liquid Wing raised a €15 Series B.

Upcoming Events… ⌛

… you can catch us at in the not-too-distant future.

… and Getting in Touch 👋.

If you’re looking for funding, you can get in touch here.

Don’t be shy, get in touch on LinkedIn or on our Website 🎉.

We are open to feedback: let us know what more you’d like to hear about 💪.