Eka’s Weekly Roundup (2 June 2023)

Issue 34 l Learnings from Climate Investors

Google hosted a demo day for its climate change accelerator yesterday in Central London. We heard from 10+ startups ranging from Pre-Seed to Series A, tackling issues ranging from circular fashion infrastructure to biodiversity mapping. To break up the pitches, Google put on an investor and founder panel to discuss the current state of the ClimateTech market with panelists from Molten, Kiko Ventures, and BeZero Carbon. We summarise our learnings below.

Optimism from Climate Investors 🗞️

The panel at yesterday’s Google Climate Change event included Tommy Ricketts from BeZero, George Chalmers from Molten, and Robert Trezona from Kiko Ventures.

There has been strong growth in the climate funding environment. The world is currently experiencing a significant shift towards a more environmentally conscious society, and this has led to a rise in the climate tech industry. The industry has seen tremendous growth, with climate tech investments more than doubling to 2.7 billion dollars in 2022. France saw the strongest fundraising amount, with the UK following second.

Green ‘discount’ is still prevalent when pitching to investors. When pitching to investors at the mid and late stages, climate companies are still receiving a green ‘discount’ compared to generalist deals in the market. Most of this is down to larger generalist funds coming down into climatetech VC such as Beyond Net Zero and Decarbonisation Partners, which have strict climate allocation mandates. This can cause a misalignment between capital raised versus the supply of start-ups that are looking for $100m tickets.

Fusion of hardware and software is becoming prominent. One trend that investors have seen is the fusion of hardware and software investing. The intersection between these two categories presents an exciting opportunity as this would be able to decarbonise heavy industry. Sifted wrote about this recently here.

Areas of interest lean towards heavy industry. There are specific areas that need solving within the climate venture, such as aviation, methanol products, and food systems. Bringing originality to these areas is crucial for startups to have a competitive edge. The level of competition in the industry is high, and startups need to stand out from the crowd to attract investors' attention.

Necessary traction varies greatly across markets. It's also important to note that traction varies within the climate venture. If a company is building a product in a category where there's already procurement, then more traction is likely. However, if a company is building something new, even into series A, then traction isn't as significant a factor. Understanding the customer's ingenuity is crucial in these cases, as you don't know what you're buying.

Week in Impact Articles ✍🏽

Monday: £650m for UK Life Sciences

Tuesday: Where food and data intersect, plus looking at UK food price controls

Wednesday: Staffing virtual wards during staff shortages

Thursday: Tony’s Mission Lock

Friday: State of GPT

3 Key Charts 📊

1. Cost of living in the UK for single people

2. Another chart on battery unit economics

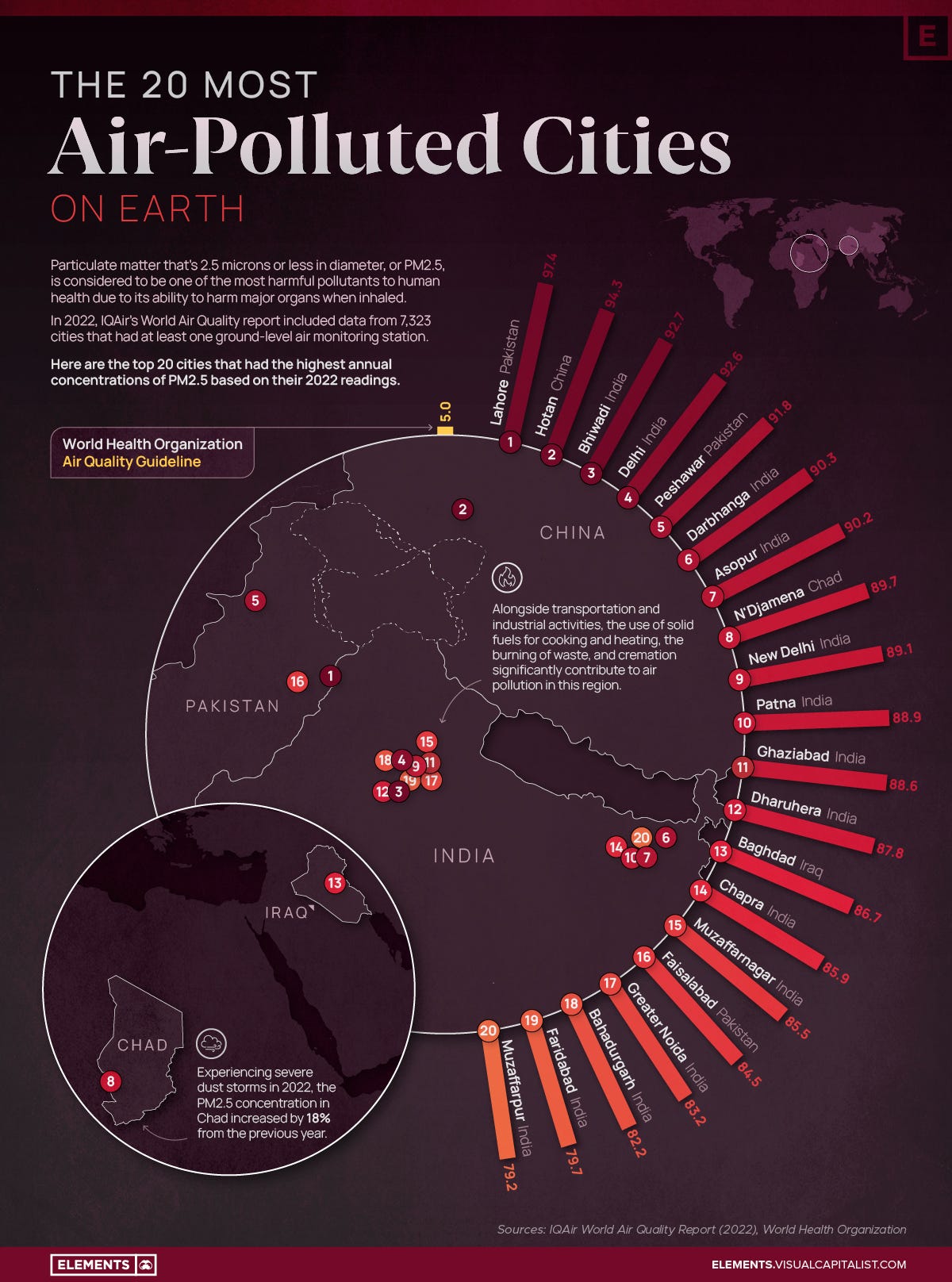

3. City air pollution worldwide - Lahore stands out

Deal Capture 💰

Deals in the impact space across the UK and Europe

Esforin

Energy trading platform raised a E7.5m Series B. Led by SEB Greentech.

Hypervision Surgical

Medical imaging startup Hypervision Surgical raised £6.5m. Included Heran Partners.

Proxima Fusion

Nuclear startup Proxima Fusion raised E7m. Led by Plural and UVC Partners.

QFlow

Construction startup QFlow raised £7.2m. Led by Systemiq.

Riverse

Carbon credit issuer Riverse raised E1.5m. Led by Speedinvest.

Getting in Touch 👋.

If you’re looking for funding, you can get in touch here.

Don’t be shy, get in touch on LinkedIn or on our Website 🎉.

We are open to feedback: let us know what more you’d like to hear about 💪.