Eka’s Weekly Roundup (18 November 2022)

Issue 9 l Slush

This week, Hamish and I headed to Slush over in Helsinki 🥶. A few highlights were the ‘mild’ temperatures of ‘only’ 0C, listening to the OnlyFans CEO, and realising much too late that Finnish PM Sanna Marin was giving a talk late yesterday evening (which we missed). On the impact side, there were a few less climate talks compared to last year (and still no dedicated health panels), but we pick out our key learnings below.

Impact at Slush 🗞️

♻️ Circular Economy: Vestiaire and Back Market

We heard from Max Bittner (Vestiaire) and Thibaud Hug de Larauze (Back Market) at the Serene Stage yesterday afternoon. The panel was on all things circularity, second-hand use, and how they both view their business impact.

👚 Fashion

On the fashion side, Max shared a few datapoints on the fashion industry around volume and consumables increases over time. In the last 20 years, the items worn per person has at least doubled. H&M and Zara produce 1b items of clothing per year, or 2b combined. All of this results in the fashion industry being the 2nd (or 3rd, depending on how you define it) worse polluting industry in the world.

Vestiaire and BCG produced a report on the potential of the secondhand market in a world of excess supply. They estimated that there were 1 trillion pieces of fashion unworn and unused in peoples wardrobes. Tapping into this supply base and encouraging reuse, rental, or second-hand selling in Vestiaire’s case could 1/ extend the theoretical LTV of the item and 2/ depreciate the negative impact of single-use production.

📱 Tech

On the tech side, Thibaud broke out the impact of new hardware products on global CO2 emissions. Of the 36b global CO2 emissions, tech products are roughly 2b of that. Within the tech contributions, 80% relates to new hardware products such as Smartphones and TVs, which is roughly 4% of total CO2 emissions.

The problem in encouraging users to switch to second-hand refurbished items, specifically in tech. He called for Apple and Samsung to release more information about how to repair hardware items for better longevity, rather than promoting upselling to >£1k items.

🤝 Common Ground?

Assets, not Consumables. One theme that both spoke about was the difference between assets and consumables. Items in a fast

fashionproduction supply chain are treated as consumables & perishables rather than long-lived assets.Secondhand needs Trust. Converting users to a different behavioural patterns requires trust. More than that, it requires superior pricing, quality, and experience compared to alternatives. That is our central thesis around scaling impact with consumers, i.e. it needs to be more enjoyable than unsustainable alternatives (and the impact is just a nice side benefit!).

Looming large Brands. Both Vestiaire and Back Market have large looming brands behind them, whether that’s the Luxury Houses or Device OEMs. The businesses need them as a theoretical initial supply base but can tap into second and third iteration TAMs beyond them, so striking the right balance of collaboration and disruption will be important.

🌎 Impact Investing: Fifty Years, David Helgason, Future Positive Capital, and Voyager

The second impact panel was with Seth Bannon from Fifty Years, David Helgason from Unity, Sofia Hmich of Future Positive Capital, and Sarah Sclarsic from Voyager. They mainly spoke about the evolution of impact investing over time, geographical differences between Europe and the US, as well as what they were most excited about (hint: quite a lot!).

Impact TAM is the entire world. Sarah pointed out the impact TAM (regardless of hype throughout 2021-22) is still larger than any other segment, with the size of the ‘entire world’. As we’d heard with the second-hand market speakers earlier, the TAM can be expanded a second or third time by increasing lifecycles beyond single use.

Three shades of impact. Seth mentioned three stages of impact. The first is decarbonisation: taking carbon out of existing processes such that future processes emit less (or no) carbon. The second is capture, where companies take carbon out of the air, which has already been emitted. The third is adaptation, which looks at solutions to live with climate change. Most VC funds focus on the first two of these.

The Mr. Burns test. Another thing Seth mentioned was 50 Years’ ‘Mr. Burns’ test. A notorious Simpsons character, Mr. Burns is famous for being an individualistic, greedy capitalist. 50 Years uses this test to see how their portfolio companies’ products fare against incumbents. A traditional sustainability view might tell you that consumers value sustainability just as much, if not more, than pricing. But most of the data shows that those consumers are in the minority. By creating a sustainable produce that even Mr. Burns would choose, companies can create scalable mass-market solutions that have sustainability as an ‘add-on’ rather than primary purchasing driver.

Climate as a global good. There was some talk around how to measure impact. Voyager has a target of 500m tonnes of CO2 during the lifetime of the fund. This can also be used in CO2 equivalent gasses such as methane. However there was also talk of climate impact as a global good beyond CO2 emissions. Impact shouldn’t always be measured at the micro or output level, and should be thought of as being fairly redistributed to all as a global good over time.

3 Key Charts 📊

1. Unpacking emissions sources from the FIFA World Cup

2. Not all tech companies are laying workers off (but most are)

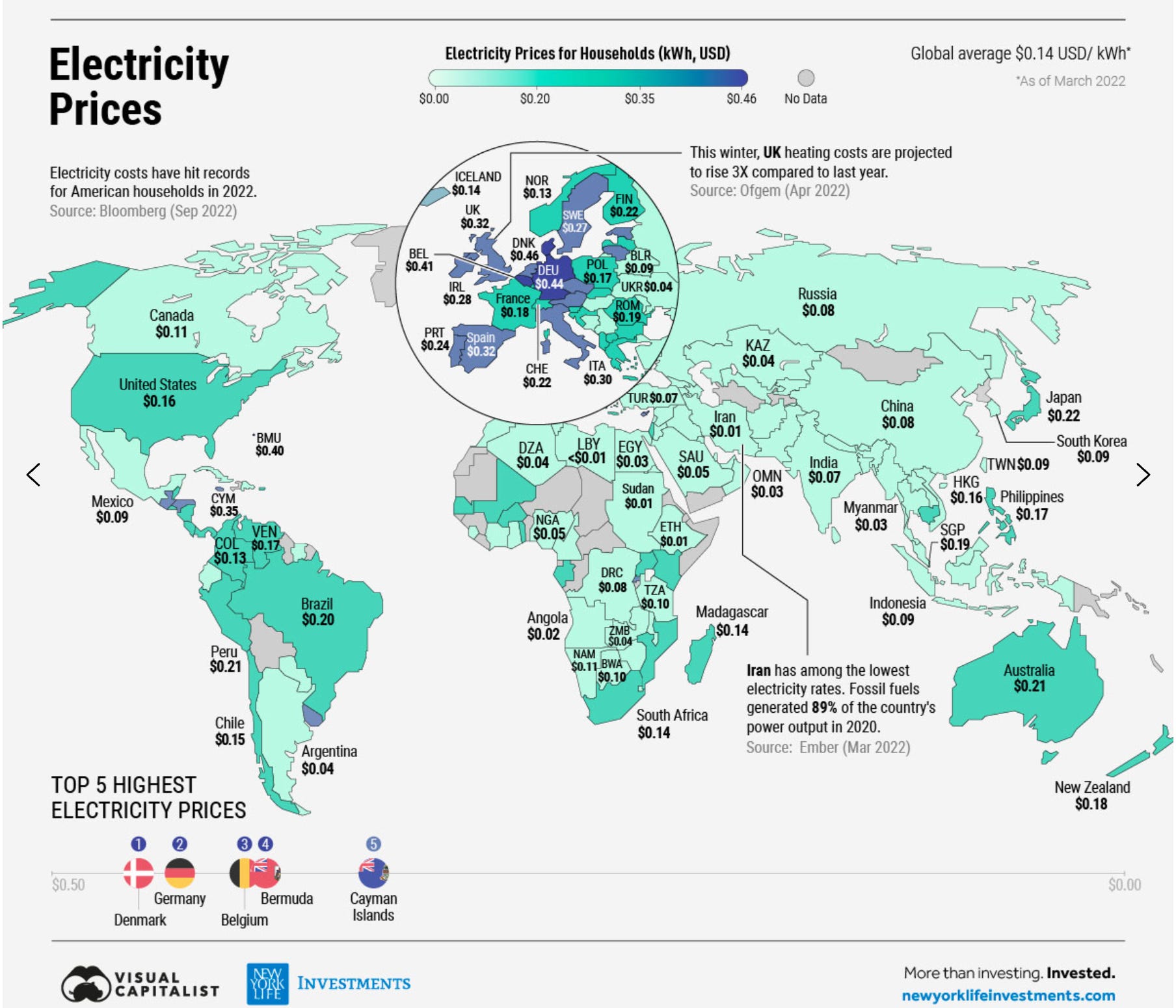

3. Charting global energy prices - Europe in the red purple

Deal Capture 💰

Deals in the impact space across the UK and Europe

Airly

Air quality platform Airly raised a $6m Series A round. Included firstminute capital and Pi Labs.

Cambridge GaN Devices

Fabless semiconductor company CGN raised £16m. Led by Parkwalk Advisors and BGF.

Circularise

Dutch blockchain startup Circularise raised €11 million Series A funding. Led by Brightlands Venture Partners.

Nofence

Agtech company Nofence raised a 130m NOK round. Led by Ferd and Sandwater.

SharpTx

Genetic disease therapeutics company SharpTx raised £3m. Included Kima Ventures, Proxy Ventures, and Headline Ventures.

Getting in Touch 👋.

If you’re looking for funding, you can get in touch here.

Don’t be shy, get in touch on LinkedIn or on our Website 🎉.

We are open to feedback: let us know what more you’d like to hear about 💪.

Thanks for another great article. The 3 shades of impact: “The third is adaptation, which looks at solutions to live with climate change.” In your opinion, what might these solutions look like? Are there insufficient businesses looking at this angle?