The macro view: headline, we crossed the 1.5C barrier

There were a few press mentions of this in early January, but I still don’t think we’ve fully grasped the significance of passing 1.5C. Yes it’s a symbolic threshold, but it was rooted in risk-adjusted views of a warming world at which point there would be dangerous and irreversible impacts on ecosystems, human health, and economies. 2C is the next threshold and looks very possible in the next 10-20 years based on the current trend line.

I love transcript data and find it a good pulse on what executives are thinking about in the corporate world. We can see a clear decrease in mentions of climate change (and that’s not linked to geopolitics or US elections).

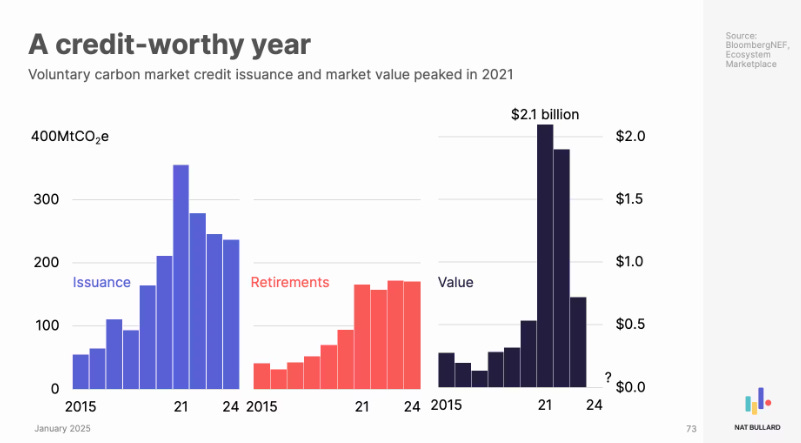

Do you remember the voluntary carbon market (VCM) hype?

The value of the VCM market has come down a great deal since 2015, though by less than the no. of issuances. This has been attributed to over supply of carbon offsets relative to demand growth.

A new lens: climate x health

We’re increasingly thinking about climate x health (see Peter Havers’ post from last week). In early January, this piece came out looking at occupational heat exposure and how it is impacting labour-intensive jobs. These are typically located in lower-middle-income and low-income economies, where in the worse case, workers perform tasks in heated conditions for up to 50% of their working hours.

Energy: generation, grid, and spend

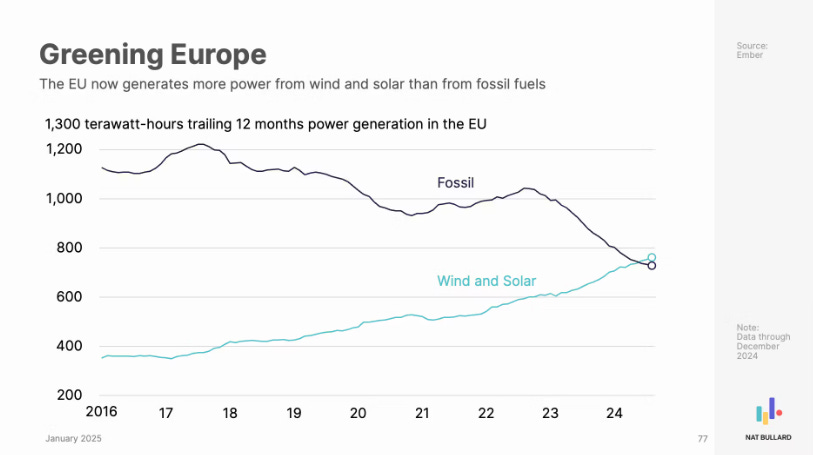

I’mr really excited about this chart. A lot needs to happen from here (i.e. batteries, or what Axle’s building around intermittency). Feels like one of the ‘few’ out-and-out positive charts in the deck and we need to shout about it!

30% YoY increase in the US is high. As of 1 year ago, the UK had one of the highest interconnection queues for solar & wind compared to Spain, Italy, and France (note Germany not included in the dataset).

This surprised me. I didn’t expect EM to have a rising % of wallet to spend on energy depending on the income decile - I wonder if this is because the 10th and 90th percentile have a much broader absolute range in advanced economies than in emerging markets which means a slight absolute change in energy consumption has a larger impact in total wallet spend.

The UK residential solar scene hasn’t been as strong (unsurprisingly) as its sunnier European neighbours. But it’s had significantly lower subsidies compared with feed-in-tariffs (France, Germany), investment grants (Spain), and tax incentives (Portugal). In that context, solar PV installation is still interesting. how

This was surprising.

We knew about China exporting deflation in green energy assets, but I hadn’t seen it visualised in this way. 250% of global energy demand feels high. I haven’t been able to sense check this in lots of depth but Reuters reported last year that China’s solar cell production capacity was 1,000 GW while demand was ‘only’ set to be 980 GW by 2035.

Batteries, batteries, batteries

Same story, different asset. 7x global demand feels wild.

Electric vehicles are becoming more and more mainstream

This is still ‘only’ looking at new car sales rather than total car parc. Cars typically get replaced every 7-10 years… estimates suggest that EVs are c.5% of China’s total car parc, so even assuming 100% EVs, it would still take quite a long time to funnel through.

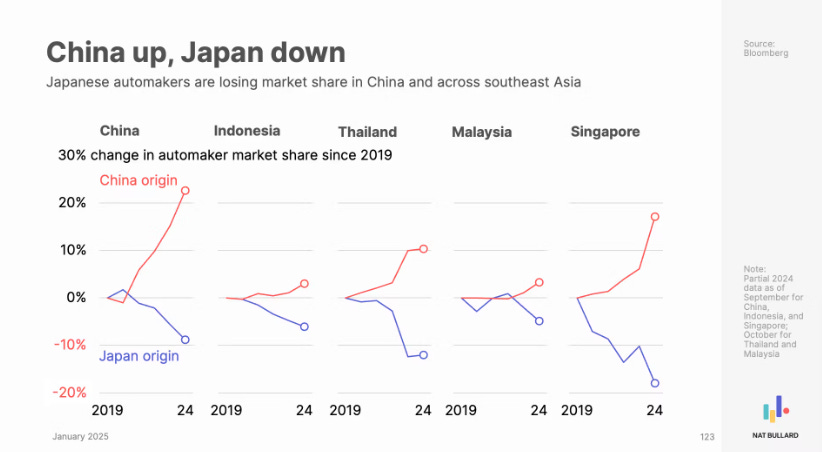

We often think about German car makers as being the worse hit and had forgotten about other players in the ecosystem.

This is the key part of the Eka climate thesis. The system can afford a price premium in the early days only if this subsidises a move towards price parity over time. Ignoring the governance concerns on Tesla for a second, this chart is such an awesome illustration of this!

Well understood in the markets, but nice to see the data visualised. Will 2025 be the year where BYD overtakes Tesla on a full-year basis?

AI x Energy???

Ireland uses about 1/5 of its energy on data centers (!). For context, the US is ‘only’ 4%. It’s come up almost x3 in less than 10 years. This is wild.

An interesting lens with which to view the ‘energy problem’, in the context of what OpenAI et al see. It’s not that big of a problem from a wallet perspective. Carbon economics (I assume) would be quite different - I haven’t yet seen comparable data here which takes into account R&D staff, and other components.

“Boring” decarbonisation

AI isn’t the only thing that needs decarbonising - I liked this section which looked at decarb beyond AI. One piece is cold chains, and another is producing goods & services more locally relative to end-consumption.