50 interesting things for climate & health in the SpaceX S-1

Issue 159 l Eka’s Weekly Roundup (3 June 2026)

⚡️ Energy & AI within the SpaceX group

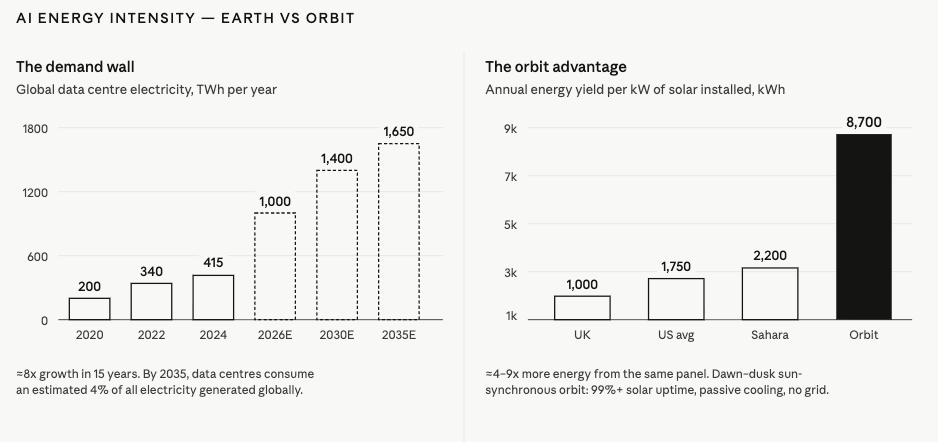

US electricity generation has been flat for 15 years, a 0.1% CAGR from 2008 to 2023. SpaceX treats that as a hard ceiling on how much AI compute the country can power. [p.3]

It calls the resulting gap an “unsustainable strain on grids, supply chains, and the environment.” [p.3]

Space-based solar produces more than 5x the energy per unit area of a ground panel: constant sunlight, no atmosphere, perfect orientation. [p.3]

The target is 100 GW a year of orbital AI compute by the late 2020s. [p.8]

That means putting roughly one million tonnes into orbit annually. Today the whole world launches about 3,000 tonnes a year. [p.8]

First orbital data centres could deploy as early as 2028. [p.2]

Do the launches use up the power they’re meant to escape?

In a recent interview, Musk made three, separate, bold claims:

Earth doesn’t have enough power for AI, so compute has to go to space;

Getting it there needs over 10,000 launches a year; and

Each launch uses about 20% of all US energy at the point of launch.

Put those together and it looks self-defeating: ten thousand launches at a fifth of US energy each would need 2,000 times the country’s entire energy supply. So either Musk is wrong, or the claim means something different.

It means something different. “20% of US energy” is 20% of US power, not a year’s worth of energy: a rate held for the two minutes a rocket is climbing, like driving 200 mph for two minutes and covering under seven miles of road. The honest figure is the fuel burned: about 14 GWh per launch, so 10,000 launches is 140 TWh a year. Against US electricity generation of roughly 4,000 TWh, that is about 3.5% of annual US electricity generation. Real, but nowhere near “we’ve used up the country.”

And it is a one-off cost. That 140 TWh launches solar-powered compute that then runs in orbit, where a panel collects five times more energy than on Earth and never sees nightfall. One terawatt of orbital compute harvests about 8,760 TWh a year, so the launch bill pays itself back in weeks. The launches don’t drain Earth’s energy, they buy access to a far richer supply (of course, if you believe that there is a payoff on the other side!). That answers Musk’s first point: the same panels simply work five times harder up there, where the sun is stronger and always on.

The one real catch: if the methane has to be clean, made from renewable electricity rather than pumped from the ground, producing 10 million tonnes a year would itself draw roughly 6% of US electricity, off the same grid Musk says is already full. The orbital compute still harvests far more than that, so the maths stays positive. But “we’re short of power on Earth” and “so let’s make millions of tonnes of rocket fuel with that power” sit awkwardly together, and that fuel question, not the launch spike, is the one worth watching.

Assumptions: 10,000 launches/year (Musk’s figure); ~14 GWh of chemical energy per launch (1,000 t methane × 50 MJ/kg); US electricity generation ~4,000 TWh/year (EIA); 1 TW of orbital compute running 8,760 hours a year. Clean-fuel case assumes power-to-gas at ~55% efficiency.

🚀 Sustainability beyond energy: rockets, Tesla integrations, and training

The data centers behind their AI bet currently run “significantly on natural gas and gas turbine technology.” [p.35]

SpaceX deployed the first gigawatt-scale Megapack battery installation in 2026: Tesla batteries paired with gas turbines, not solar. [p.7]

Risk factor explicitly mentions “environmental effects of emissions and other byproducts from rocket launches in Earth’s upper atmosphere.” [p.33]

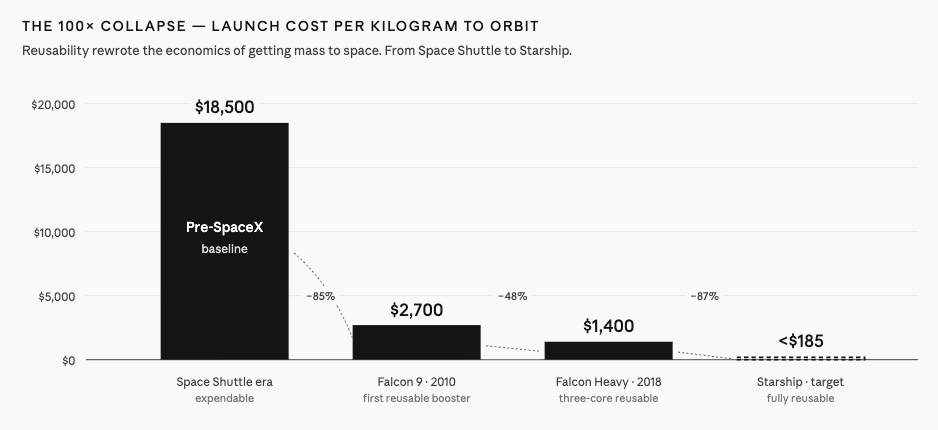

Launch cost trajectory: $18,500/kg historical → $2,700/kg (Falcon 9, 2010) → $1,400/kg (Falcon Heavy, 2018) → target <$185/kg (Starship). [p.75]

Starlink does 1,000+ automated collision-avoidance maneuvers per day: orbital debris is becoming an operating cost. [p.8]

Starlink satellites account for ~75% of all active maneuverable satellites in orbit. One company, three-quarters of the global manoeuvring fleet. [p.5]

Anthropic signed a cloud-services agreement on 3 May 2026 for the full 300 MW of COLOSSUS I at $1.25B/month (reduced during the May–June ramp). The S-1 frames it as a “monthly fee through May 2029” (~$15B/yr, up to ~$45B), but on 28 May Musk publicly downgraded the commitment to a 180-day lease with rolling 90-day mutual cancellation: so the $45B is a notional run-rate, not contracted revenue. [p.13]

How SpaceX manufactures at industrial scales

They brought COLOSSUS online in 122 days by repurposing an existing factory shell. [p.7]

COLOSSUS II came online in 91 days: industry benchmark for a 100MW greenfield DC is ~2 years. [p.7]

Terafab: chip-manufacturing JV with Tesla and Intel; long-term target of 1 terawatt of compute hardware per year. [p.9]

Starship designed for “multiple launches per day” once the booster catch tower works at scale. [p.5]

Mass to orbit by year: 1,210t (2023) → 1,699t (2024) → 2,213t (2025): ~83% growth in 2 years. [p.22]

🛰️ Equity & the digital divide through mobile connectivity

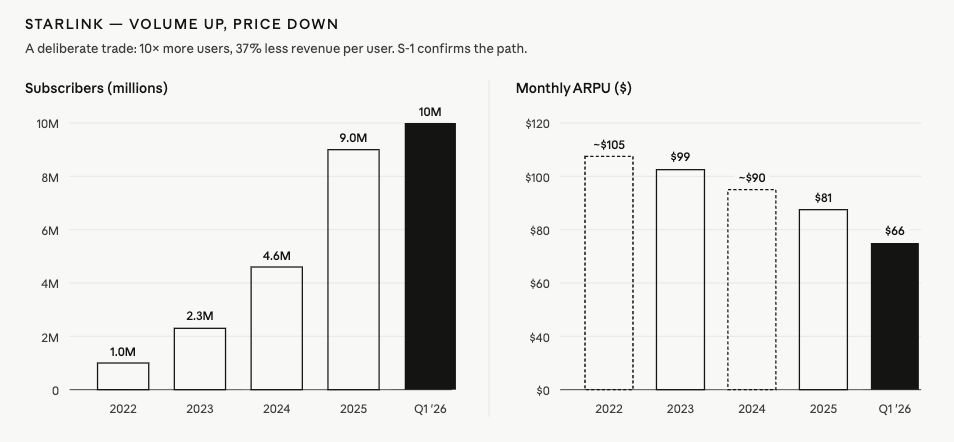

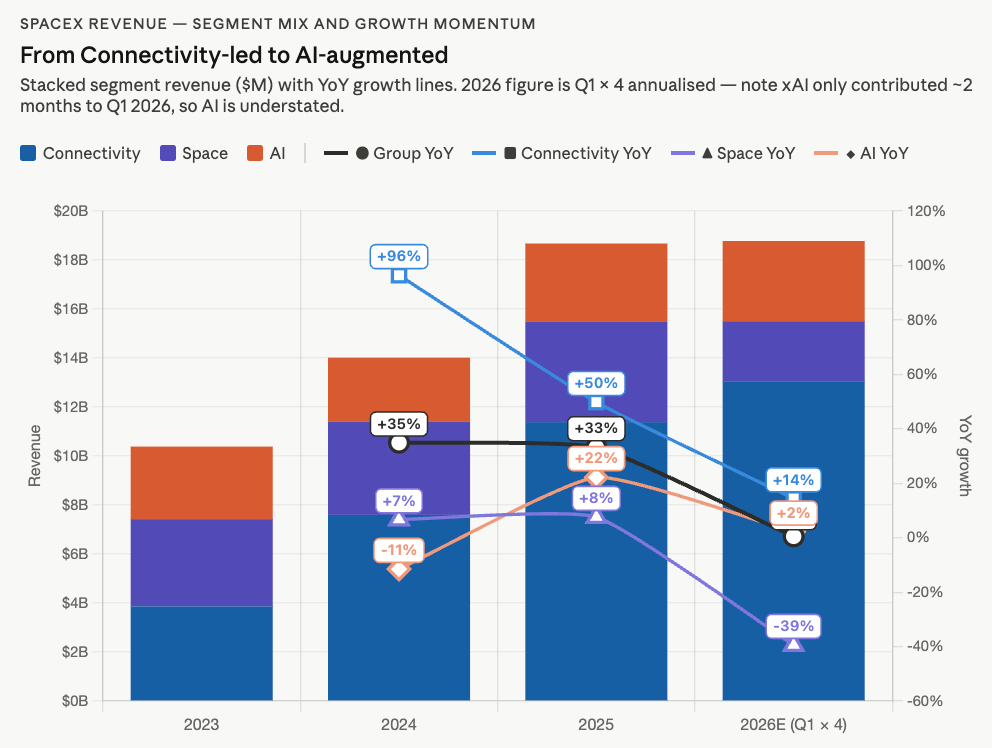

Starlink subs roughly doubled across 2025 (≈4.6M → ≈9M) but adds are now decelerating (10.3M by Q1 2026), and ARPU fell ~18% to ~$81/mo from 2023–25 as the mix shifts downmarket. So subscriber growth overstates revenue: Connectivity grew ~50% to $11.4B in 2025: strong, but well short of the subs trajectory, and the gap widens as ARPU keeps sliding. [p.1, p.23]

Service covers 164 countries, territories and markets: a population of 3.3 billion people in those geographies. [p.1]

ARPU is falling fast: $99 (2023) → $66 (Q1 2026), reflecting a mass-market downmarket shift. [p.23]

Stated aim: connect “over three billion unconnected people” to the internet. [p.3]

Starlink Mobile (direct-to-cell) covers ~30 countries, ~7.4M monthly unique devices. [p.1]

Starlink credited with keeping survivors connected during multi-week comms outages from flooding. [p.137]

🤖 Health & human augmentation through AI products

“Digital human augmentation” is listed as a near-term AI segment growth strategy. Wording is deliberately vague. [p.10]

Grok-5 is currently being trained at COLOSSUS II. [p.12]

117M MAUs used Grok’s AI features as of Q1 2026: large-scale AI exposure for a single tool. [p.2]

1.3 billion active accounts across Grok + X; 550M MAUs; 350M daily posts feeding training data. [p.84]

Bio/biotech is essentially absent from the S-1: striking gap given the AI-for-science framing. [observational]

🪨 Materials & in-house design across manufacturing

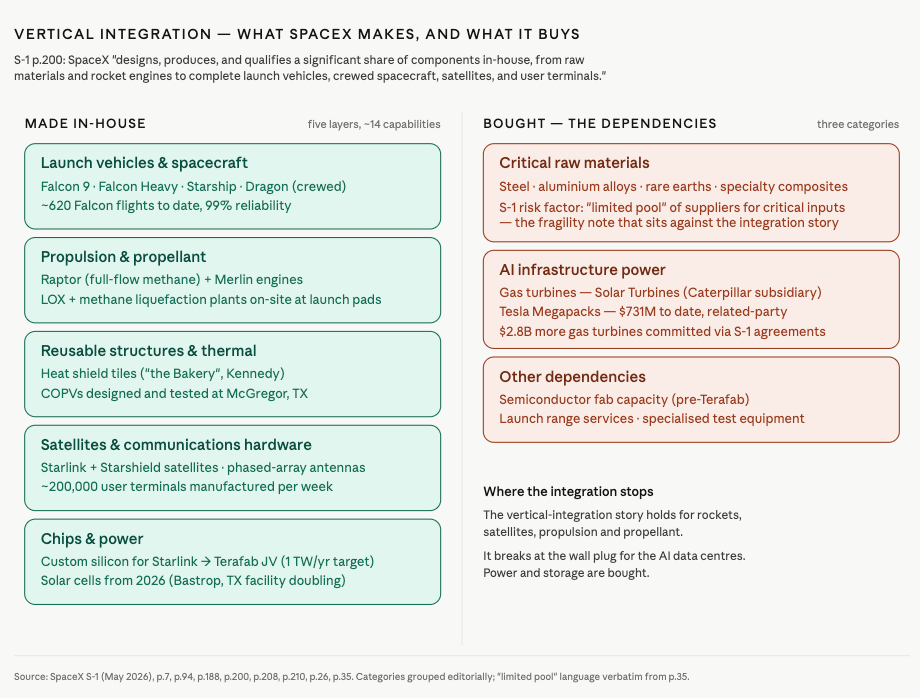

The S-1’s exact phrasing: SpaceX “designs, produces, and qualifies a significant share of components in-house, from raw materials and rocket engines to complete launch vehicles, crewed spacecraft, satellites, and user terminals.” [p.200]

Heat shield tiles are made in-house at “the Bakery”: a dedicated facility on Kennedy Space Center, Florida. Designed for repeated high-velocity reentries (not single-use like Shuttle tiles). [p.210]

Raptors are full-flow staged-combustion engines burning cryogenic methane + oxygen: only the third such engine ever to fly. Methane choice matters because it can theoretically be synthesised on Mars from CO₂ and water. [p.188]

Phased-array antennas designed, fabricated and scaled in-house: silicon, hardware, software, manufacturing, fulfillment all under one roof. They produce ~200,000 user terminals per week. [p.94]

Propellant is also made on-site: air separation units (for liquid oxygen) and methane liquefaction plants co-located with launch pads. Most launch providers buy propellant; SpaceX makes its own. [p.26]

The Bastrop, Texas facility is being doubled in 2026 to add gateway antennas, solar cells, and AI compute satellites: SpaceX is quietly becoming a PV manufacturer. [p.210]

💰 Capital & returns picture

One caveat that reframes every YoY number below: 2025 and prior periods are recast to include xAI (acquired 2 Feb 2026) and X (March 2025) under common-control accounting (this is normal). The $18.7b revenue number in 2025 line is xAI-inclusive; standalone SpaceX was ~$15.5b.

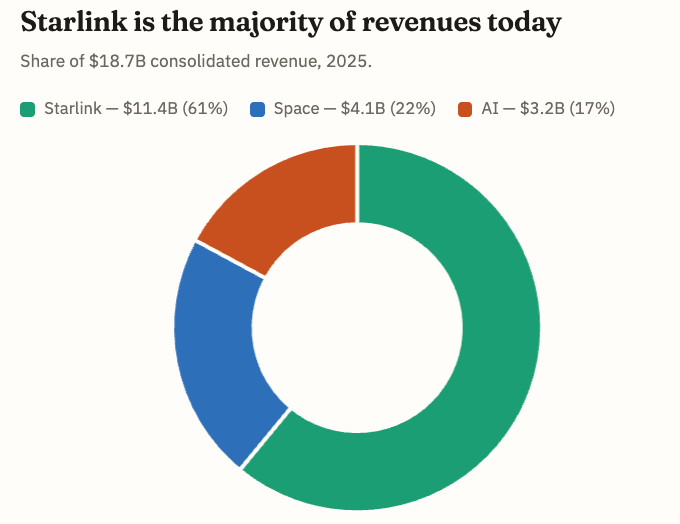

2025 revenue: $18.7b. Net loss: $4.9b. Adjusted EBITDA: $6.6b. Starlink is c.61% of revenues, Space is 22%, and xAI is 17% of revenues (we’ll talk about cash usage later!). [p.2]

Revenue compounded $10.4b (2023) → $14.0b (2024) → $18.7b (2025): +33% YoY at the group level. Within this, Starlink grew +50% YoY but its run-rate is slowing given lower ARPU, Space grew +8% YoY but this is also slowing (although lumpy line!).

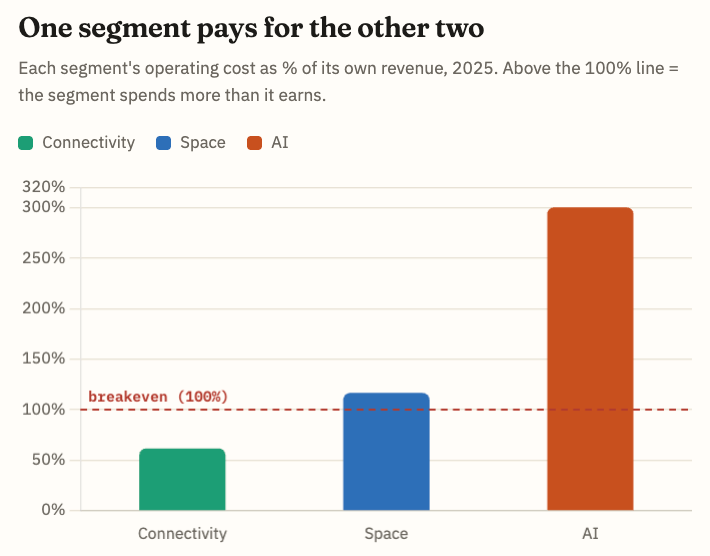

Connectivity (Starlink) is the only profitable segment: $4.4b operating income on $11.4b revenue in 2025, growing 50% YoY.

The AI/”SpaceXAI” segment lost $6.4b from operations on $3.2b revenue in 2025: but most of that “revenue” is legacy X advertising (~$1.8b, down $100M YoY), not Grok. The burn is accelerating: Q1 2026 alone lost $2.5Bb on $818m revenue.

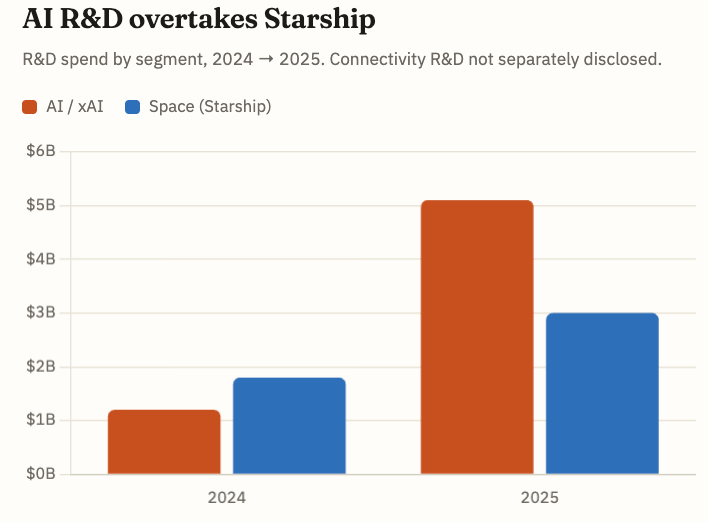

AI R&D quadrupled in a year: $1.2b (2024) → $5.1b (2025). [p.95]

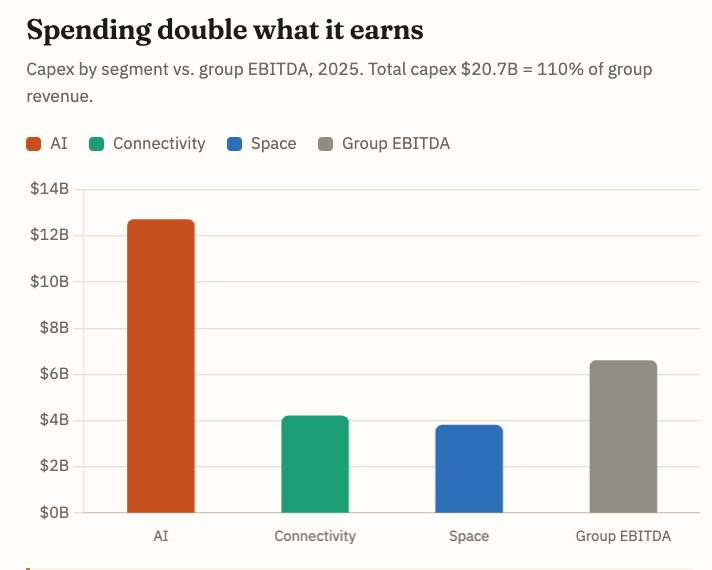

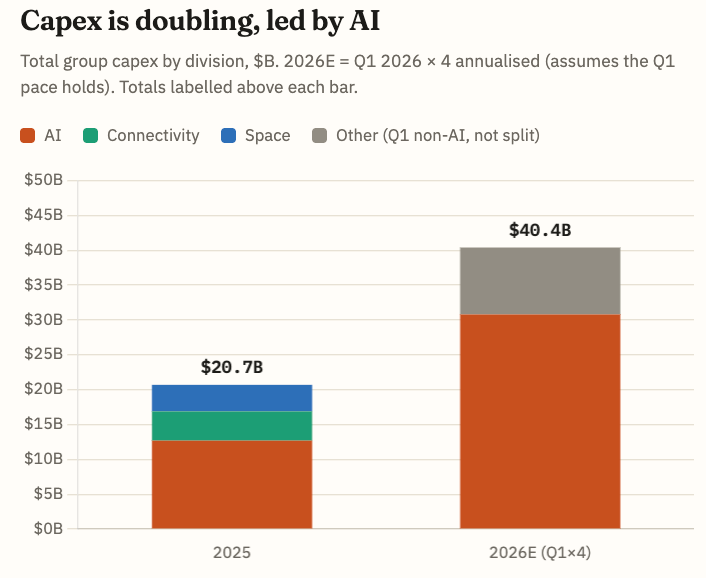

AI capex was $12.7b in 2025: ~60% of group capex, and more than Space ($3.8b) and Connectivity ($4.2b) combined. It’s accelerating, not stabilising: Q1 2026 AI capex was $7.7b in a single quarter (~$30b annualised). Read this against the Feb 2026 xAI close: the 2025 figure is recast, but the Q1 run-rate is the first “real” combined quarter, and it’s where the cash is going. [p.22]

Total capex hit $20.7b in 2025 (110% of group revenue); another $10.1b in Q1 2026 alone. [p.22]

Total assets doubled in 15 months: $57b (end-2024) → $102b (Q1 2026), largely xAI. [p.22]

Space is roughly breakeven as reported (−$0.7b), even while carrying $3b of Starship R&D.

Cash on hand dropped from $24.7b (end-2025) to $15.9b (Q1 2026): burn rate is now significant. [p.22]

SpaceX raised ~$10b+ of VC over its life, but the ~$10bB asset base isn’t purely equity magic: there’s ~$29b of principal debt, a March 2026 Morgan Stanley bridge loan and $1.9b of 2025 interest expense, the ~$14b 2025 capex gap was plugged with debt + preferred, and the jump to $102b is mostly the all-stock xAI merger (~$250b paper value): not cash raised. Accumulated deficit is ~$41b. [p.84, p.22]

At $1.25b/month the Anthropic deal annualises to ~$15b: ~80% of all 2025 group revenue: but Musk recharacterised it on 28 May as a 180-day lease with rolling 90-day mutual cancellation, terminable if SpaceX’s own compute gets tight. So it’s a notional run-rate, not contracted revenue. [p.13]

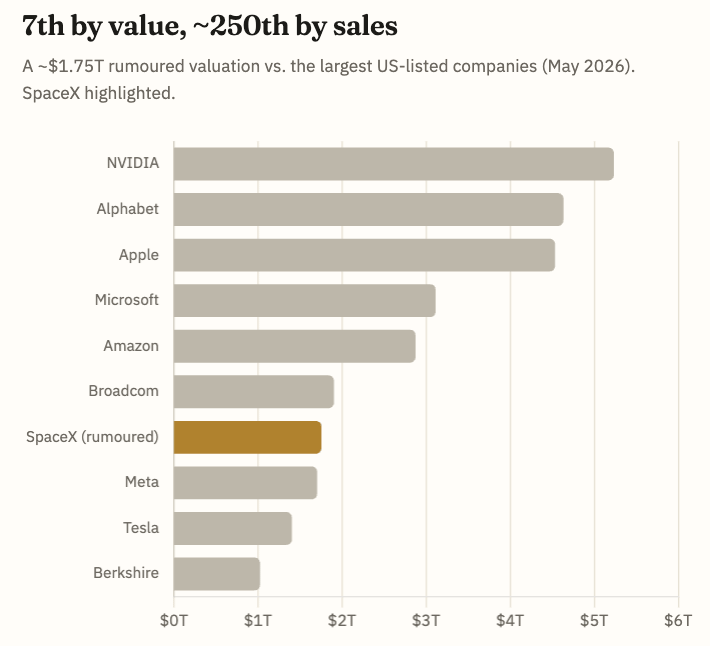

Rumoured combined IPO EV (SpaceX + xAI + X) is ~$1.75 trillion: ~94× 2025 revenue, ~400× the only profitable segment’s operating income.

Use of proceeds: AI compute infrastructure, launch infrastructure, satellite constellations, general corporate. [p.67]

One note to close: the use of proceeds maps almost exactly onto where the cash is already going: AI compute, then launch and satellites. With Starlink the only profitable segment (+$4.4b) and group capex running at ~$10b a quarter, the IPO is essentially asking public markets to keep funding the cross-subsidy: a profitable connectivity business underwriting launch and AI bets that don’t yet pay for themselves. It works if orbital compute and Starship eventually convert that spend into Starlink-like economics: it’s a moonshot in the public markets!

This source of energy might save America and AI usage. But how about the rest of the world!?🤔